Introduction

Most advisors have experienced it: a client calls in a panic during a market downturn, ready to abandon a plan they agreed to just months earlier. Not because the strategy was wrong — but because they didn't truly understand it.

According to YCharts' 2024 Advisor-Client Communication Survey, 75% of clients either switched or considered switching advisors in 2023, and only 64% of typical advisor conversations resonated with clients — down from 70% the prior year. That gap between what advisors communicate and what clients actually retain is where relationships break down.

Client education is the foundation of trust, retention, and long-term growth. Educated clients stay committed during volatility, follow through on recommendations, and are far more likely to refer others. Closing that communication gap starts with a repeatable approach — and that's exactly what this article covers.

Key Takeaways

- Tailor education to each client's life stage, goals, and preferred format

- Use clear visuals paired with plain-language context to simplify complex concepts

- Address behavioral biases proactively, well before market volatility forces the conversation

- Host group workshops to build trust and reach prospects at scale

- Embed brief educational moments into every client touchpoint, not just annual reviews

Approach 1: Personalize Education to Each Client's Needs

Age, wealth stage, financial confidence, and risk tolerance all shape what a client needs to hear — and how they need to hear it. Generic education misses the mark for most of them.

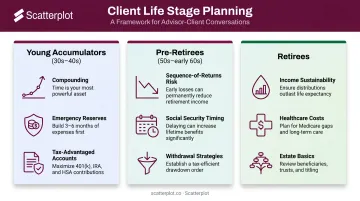

Segment by Life Stage

The education a 32-year-old saving for a first home needs looks nothing like what a 58-year-old managing a drawdown strategy needs. Consider these practical differences:

- Young accumulators (30s–40s): Focus on compounding, emergency reserves, and tax-advantaged accounts. Keep it goal-specific and forward-looking.

- Pre-retirees (50s–early 60s): Shift to sequence-of-returns risk, Social Security timing, and withdrawal strategies. Cerulli research found that advisor reliance rises sharply as retirement nears — from 27% before retirement proximity to 57% at retirement — meaning these clients need more substantive guidance, not less.

- Retirees: Income sustainability, healthcare costs, and estate basics become central. Confidence in the plan matters more than technical detail.

Match the Format to the Client

YCharts found clients prefer email (61%), phone (41%), and one-on-one meetings (38%) — and virtual meeting use nearly doubled from 20% to 38% between 2023 and 2024. Younger clients skew heavily toward virtual; pre-retirees often want phone or in-person. Offering a mix ensures the information actually reaches people in the format they engage with.

A few practical steps:

- Ask new clients directly how they prefer to receive information

- Offer the same key concept in two formats when stakes are high (for example, a brief written summary plus a chart)

- Avoid assuming that more detail equals more value — for many clients, a one-page plain-language summary outperforms a 12-slide deck

Ditch the Jargon

Terms like "standard deviation," "duration risk," or "alpha" create distance rather than clarity. When a client hears something they don't understand, they often won't ask — they'll just disengage.

The fix is connecting every concept to something concrete: instead of "your portfolio has a modified duration of 5.2," say "if interest rates rise by 1%, the bond portion of your portfolio would lose roughly 5% in value — here's how that affects your income plan."

Approach 2: Use Visual Communication to Make Complex Concepts Clear

No paragraph can do what a well-constructed chart does in seconds. Visuals don't just decorate financial conversations — they anchor them. A client who can see that markets have recovered from every major downturn over the past 50 years will respond differently to a correction than one who has only been told it.

The Right Visual for the Right Anxiety

Different client concerns call for different types of visuals:

- "Am I diversified?" — asset allocation charts show what a client owns and why each piece belongs

- "Should I be panicking right now?" — historical market return charts put the current moment in perspective

- Inflation impact comparisons address why purchasing power matters more than a raw account balance

- "Am I still on track?" — scenario projections connect today's volatility to the long-term retirement picture

The key is matching the visual to the conversation, not just pulling something generic from a news source. A chart ripped from CNBC carries CNBC's narrative — not yours. It lacks the client's context and your firm's positioning — and it often raises more questions than it answers.

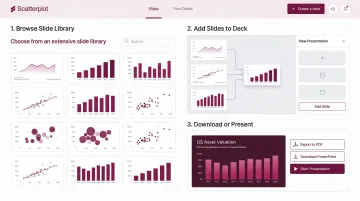

How Scatterplot Solves the Prep Problem

Building polished, branded visuals from scratch takes hours most advisors don't have. Scatterplot addresses this. The platform gives advisors access to a library of daily-updated, client-ready investment charts and slides — automatically refreshed as market data changes, and customized with the firm's logo, colors, and compliance disclosures.

The workflow is straightforward:

- Browse the slide library and select charts that fit the client conversation

- Add slides to your deck — the platform automatically keeps data current, no manual updates needed

- Download as a PDF or present directly from the platform

Each slide comes with guided talking points, so advisors can walk into any client meeting with both polished visuals and a clear narrative — without spending the morning building a deck. At $99/month, with a 7-day free trial to test it before committing, the subscription covers unlimited access to the full slide library — daily updates included.

Visuals Open the Conversation — Advisors Close It

A chart is a starting point, not a conclusion. The advisor's job is to connect what the client sees to what it means for their plan. "This chart shows how markets have historically behaved during rate hike cycles — here's why your current allocation is positioned the way it is given that backdrop." That combination of credible visual plus personalized interpretation is what builds confidence.

Approach 3: Help Clients Recognize and Overcome Behavioral Biases

Financial decisions are rarely purely rational — and that's not a character flaw. It's how human cognition works under uncertainty. Advisors who acknowledge this openly tend to build stronger, more trusting client relationships.

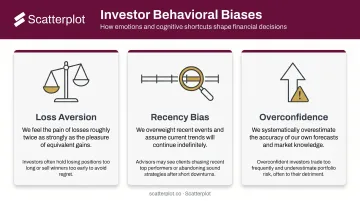

Three Biases Worth Addressing Proactively

Per CFA Institute's behavioral finance framework, the most common investor biases fall into two categories — cognitive errors and emotional biases. Three worth naming explicitly with clients:

- Loss aversion: Losses feel roughly twice as painful as equivalent gains feel good. This causes clients to over-react to short-term declines.

- Recency bias: Recent market events get overweighted when forming expectations. After a strong bull run, clients assume it continues; after a correction, they assume further losses.

- Overconfidence: Strong markets can make clients feel their instincts are infallible. Left unchecked, that confidence leads to unnecessary risk-taking or departing from the agreed plan at exactly the wrong moment.

Frame It as Normal, Not Shameful

The worst way to introduce behavioral bias education is to make a client feel foolish for having emotions about money. The better frame: "This is something even experienced investors struggle with. Our job is to build a process that protects you from these patterns before they cost you."

Normalize the response, then redirect to the plan. The goal is a process that keeps emotion from driving decisions — not a client who never feels anything.

Pre-Educate Before Volatility Hits

The most effective time to walk a client through what a 20% market correction looks and feels like is before one happens. YCharts found that clients contacted frequently report 71% confidence in their financial plan during a recession, versus just 22% among rarely contacted clients — a gap driven not by portfolio performance, but by communication.

Advisors who do this work upfront spend far less time talking clients off ledges when markets actually move.

Approach 4: Host Workshops and Group Learning Events

There's something that happens in a room — or a Zoom — of 15 people learning about retirement income together. Clients who wouldn't ask a question one-on-one will ask it when someone else does first. The shared experience reduces the shame of not knowing, and that openness accelerates learning.

Formats That Work

- In-person seminars at a local venue on focused topics: estate planning basics, Social Security timing, or navigating market volatility

- Virtual webinars — lower barrier to attendance, easier to repurpose as recordings

- Employer-sponsored financial wellness sessions — a strong channel for reaching younger accumulators at scale

- Client-invite-a-friend events — Schwab's 2021 RIA Benchmarking Study found these were used by 41% of top-performing firms and generated leads for 75% of firms running prospect-only virtual events

Kitces research found seminars carried a 1.6 median marketing efficiency ratio, meaning revenue generated exceeded marketing cost — making group education one of the stronger practice-building investments available.

Show, Don't Sell

The quickest way to lose a room is to pivot from education to pitch. Attendees came to learn, not to be sold. Advisors who provide genuine, relevant insight — without a product push — leave with credibility, follow-up meeting requests, and often referrals. Those who try to close business during the event usually leave with neither.

The formula is straightforward: pick a topic your ideal clients genuinely worry about, teach it thoroughly, and let the relationship follow naturally from there.

Approach 5: Make Client Education a Continuous Practice

A single onboarding presentation doesn't create an educated client. Neither does one great webinar. Knowledge fades, circumstances change, and markets introduce new questions constantly. Education needs to be woven into every touchpoint — not reserved for annual reviews.

Embed It Into Regular Meetings

Rather than treating education as a formal agenda item, open each review meeting with one brief market or planning concept tied to something the client is currently experiencing. If inflation is in the headlines, spend three minutes connecting it to their real return targets. If rates just moved, explain what it means for their bond allocation.

These moments don't need to be long — they need to be relevant. A single well-placed concept that connects directly to the client's situation does more than a 20-minute presentation on a topic they can't relate to.

Between-Meeting Communication Matters

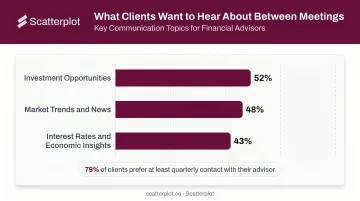

79% of clients prefer advisor contact at least every three months, yet 37% report infrequent or rare communication from their advisor. That gap is a retention risk — and a straightforward one to close.

Consistent between-meeting outreach — a brief market commentary, a chart with a plain-language caption, or a short explainer on a current event — keeps clients connected to their plan without requiring a full meeting. Scatterplot's daily-updated slides and "The Plot" market insight content address this directly: advisors can pull a current, branded visual with talking points and send it as a PDF or email attachment in minutes, without building anything from scratch.

Clients most wanted to hear their advisor's perspective on:

- Investment opportunities (52%)

- Market trends and news (48%)

- Interest rates and economic insights (43%)

That's a clear content brief for any advisor wondering what to communicate between meetings.

Use Market Headlines as Teaching Moments

When markets make news, proactive outreach that explains what's happening — and what it means for the client's specific plan — reinforces the client's confidence in their plan and in you. The numbers back this up: 88% of clients said more frequent or personalized communication would influence them to maintain their advisor relationship, and 89% said it would influence them to recommend their advisor to others.

Advisors who make education a consistent habit — not an occasional event — build the kind of relationships that hold through market volatility and generate referrals organically.

Disclaimer

The content on this site is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. It should not be relied upon as the basis for any investment decision. Past performance is not indicative of future results. Always consult a qualified financial professional before making any financial decisions.

Frequently Asked Questions

Why is client education important for financial advisors?

Educated clients are more likely to stay committed during volatility, trust recommendations without second-guessing, and refer people in their network. Client education directly affects retention, referral rates, and assets under management — which makes it a business priority with measurable impact on growth.

How often should financial advisors educate their clients?

Education should be ongoing and built into every client interaction. Brief educational moments belong in each review meeting, with proactive outreach during market events or major life changes. Research supports quarterly touchpoints as the minimum cadence — annual contact isn't enough.

What topics should financial advisors prioritize when educating clients?

Focus on what's most relevant to each client's situation: market volatility, portfolio strategy, tax considerations, and long-term planning principles. Connecting education to the client's own goals — rather than abstract market theory — keeps engagement high and reinforces trust in the relationship.

What is the 80/20 rule for financial advisors?

In client meetings, the 80/20 rule often refers to spending 80% of the time listening and asking questions versus 20% presenting. This ensures education addresses what the client actually needs rather than defaulting to a prepared one-way information transfer.

What are the 5 P's of finance?

The 5 P's are People, Process, Product, Price, and Performance. The most effective client education strategies address all five dimensions — not just product or performance — because clients evaluate their advisor relationship across each one.