The real question isn't whether you're busy — it's whether that busyness reflects a workflow problem that technology could solve. Not every inefficiency signals a need for new tools, but some patterns are clear indicators that the status quo has real costs attached.

This post identifies the specific, observable signals that tell wealth managers and financial advisers it's time to adopt or upgrade their technology — before the gap between what you're delivering and what clients expect becomes a competitive liability.

Key Takeaways

- Advisers spend roughly half their time on non-client work — the right technology shifts that balance toward revenue-generating activity

- Fragmented data and manual reporting are the most consistent operational red flags

- Client expectations for digital access have risen — and the gap shows up in retention before most advisers catch it

- Competitive and regulatory pressure has made technology adoption a baseline requirement, not a differentiator

- Define what "better" looks like before evaluating any specific platform

Why Timing Your Tech Adoption Matters

Kitces Research found that lead advisers average 43 hours per week, with barely 20% of that time spent in client meetings and no more than 50% on direct client-facing activity. The remaining hours go to administration, meeting prep, reporting, and operational tasks — work that keeps the business running but doesn't deepen client relationships.

This is a structural problem, not a personal one — and late adoption makes it worse over time. Every month spent manually assembling reports or hunting for current market data is a month where:

- Capacity isn't growing

- Service quality stays inconsistent

- Competitors with better tools gain ground

The 2025 WealthStack Study found only 38% of respondents were "very satisfied" with technology ROI — down from 44% the prior year. That figure matters because it means adopting tools indiscriminately doesn't work either. The goal is identifying the specific moments where manual processes are no longer sustainable — and where a targeted investment delivers a measurable return.

Operational Red Flags: Signs Your Workflow Is Holding You Back

Indicator 1 — Manual Data Assembly Is Consuming Meeting Prep

The scenario: two hours before a client review, you're still building slides. Sourcing current market data, creating charts, formatting decks, updating disclosures. Then it happens again for the next client, and the one after that.

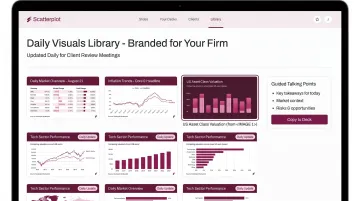

Across a 50-client book, this time cost isn't incidental — it's structural. And it's entirely addressable. Platforms like Scatterplot are built specifically to eliminate this bottleneck, delivering a daily-updated library of branded investment visuals with guided talking points so advisers can walk into meetings prepared to have a conversation rather than present a deck they just finished building.

Indicator 2 — Lack of Standardized Processes Is Creating Inconsistency

When every team member handles client prep differently, two problems emerge: onboarding new staff takes longer (because there's no process to transfer), and deliverable quality varies in ways clients notice even if they don't articulate it.

This is a systems problem, not a people problem. Inconsistency at scale is a signal the firm has grown beyond what informal workflows can sustain.

Indicator 3 — Data Lives Across Too Many Disconnected Tools

The WealthStack Study found 64% of firms cite data or real-time data access issues as a challenge — up 10 percentage points year over year. Advisory firms now operate across 11 distinct technology business areas on average. When data needs to move between systems, that fragmentation creates daily friction:

- Advisers spend hours reconciling spreadsheets, CRM records, and standalone reports instead of advising

- 61% of advisers identify "bad data" as their primary daily-work challenge (Advisor360, 2024 Connected Wealth Report)

Indicator 4 — Your Reporting Cycle Is Too Slow to Be Useful

Portfolio reports prepared infrequently, relying on manual data input before each review, mean advisers are consistently working with stale information. That creates two problems: decisions get made on outdated context, and clients sense the lag even without understanding the cause.

Real-time or near-real-time reporting isn't a luxury — it's the baseline for confident advisory conversations.

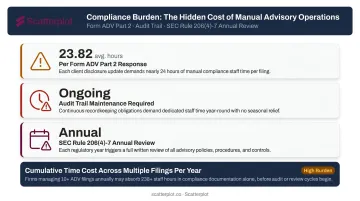

Indicator 5 — Compliance Documentation Is a Recurring Fire Drill

The SEC estimates an average burden of 23.82 hours per Form ADV Part 2 response. That's one filing. Add ongoing audit trails, disclosure management, and the annual compliance program review required under SEC Rule 206(4)-7, and the total burden on a manually run operation is substantial.

When compliance feels like an emergency every time it comes up, the firm has outgrown its infrastructure. Left unaddressed, that gap creates operational risk and adviser burnout — and rarely resolves on its own.

Client Experience Signals: What Clients Are Already Telling You

Indicator 6 — Clients Are Asking for More Access

When clients start asking where they can log in to check their holdings, or comparing your communication cadence to fintech apps they use daily, that's not a complaint — it's a signal. J.D. Power's 2025 U.S. Wealth Management Digital Experience Study formally benchmarks satisfaction with wealth management digital experiences, confirming that digital access is now a measurable dimension of client satisfaction — not a bonus feature.

Indicator 7 — Client Retention Is Slipping Without an Obvious Reason

Attrition that gets attributed to investment performance or relationship drift often has a quieter cause: the client experience simply wasn't keeping pace with expectations. The contributing factors tend to be gradual:

- Delayed or infrequent reporting

- Inconsistent communication across touchpoints

- Generic presentations that don't reflect the client's actual situation

J.D. Power's research identifies communication quality and advice delivery as primary drivers of investor satisfaction — and when those slip, so does retention.

Indicator 8 — You're Losing Prospects to More Digitally Capable Competitors

When prospects repeatedly choose firms with more polished presentations, client portals, or cleaner digital touchpoints, the issue has moved beyond internal operations into business development. A prospect comparing two advisers with similar investment philosophies will notice presentation quality, response speed, and digital access — often before they evaluate track records.

Indicator 9 — Meeting Quality Is Inconsistent Across Your Client Book

High-value clients get polished, prepared engagements. Smaller accounts get less. That gap rarely reflects a deliberate segmentation strategy. It's a capacity constraint, and clients on the receiving end notice it.

Technology should make consistent quality scalable. Scatterplot's automated, daily-updated slide library means an adviser serving 80 clients can deliver the same standard of preparation to every one of them, not just the top 20 by AUM.

Market Pressure Indicators: When the Competition Forces Your Hand

External competitive forces are compressing the timeline for advisers who are still waiting to modernize. Three pressures stand out:

Fintech and Robo-Adviser Competition

U.S. robo-adviser assets reached an estimated $634B–$754B in 2024 (Morningstar), against a $36.8T retail market. Robo-advisers aren't displacing human advisers at scale — 71% of millennials say their portfolio is too complex for a robo-adviser (RBC Clearing & Custody). What they have done is reset client expectations for what a polished, digital-first experience looks like.

The $84 Trillion Generational Transfer

Cerulli projects $84.4 trillion in U.S. wealth transfers through 2045, with more than $53T flowing from Baby Boomer households. The beneficiaries — millennials and Gen X — expect digital-first interactions as a baseline. Advisers without modern client communication tools risk losing inherited assets before a relationship is established.

Mounting Regulatory Complexity

FATCA compliance, data privacy frameworks, and the SEC's annual compliance review requirements are creating documentation burdens that manual workflows can't absorb at scale. For many firms, regulatory pressure alone is enough to make the technology decision urgent.

What Capabilities to Prioritize When You're Ready to Act

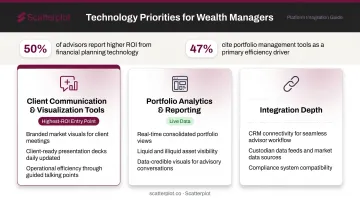

Not all technology investment produces equal returns. According to the WealthStack Study, financial planning tools and portfolio management platforms deliver the highest ROI at 50% and 47% respectively. When evaluating where to start, focus on these three categories:

Client communication and visualization tools. This is often the highest-ROI entry point for advisers still building out their technology stack. Tools like Scatterplot — which delivers a dynamic library of daily-updated, branded market visuals with guided talking points — address both operational efficiency and client experience in one solution.

Portfolio analytics and reporting. Prioritize platforms that consolidate portfolio views in real time, covering both liquid and illiquid assets. This ensures everything a client owns is visible and discussable in every review meeting.

Integration depth. A new platform that doesn't connect to your existing CRM, custodian feeds, or compliance systems creates fragmentation, not clarity. Evaluate integration capability before committing — some tools work best as a focused layer on top of existing infrastructure rather than an all-in-one replacement.

A Simple Readiness Check Before You Commit

Before evaluating specific tools, ask yourself:

- Where does the most time disappear each week — and is it client-facing or operational?

- Which client touchpoints feel most inconsistent right now?

- What do departing clients or lost prospects say when they give feedback?

- Where does the team most frequently have to improvise because no process exists?

- Is the current setup scalable, or does growth mean proportional increases in manual work?

Once you've worked through these questions, the answers should point to a specific gap — and the indicators in this article should map directly to it. If a platform doesn't address the inefficiency you've identified, it's not the right tool yet.

Before you buy, define what "better" actually looks like — hours saved per week, client satisfaction scores, number of plans produced, or revenue per client. Without a baseline, ROI is impossible to measure and adoption motivation erodes without one.

Disclaimer

The content on this site is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. It should not be relied upon as the basis for any investment decision. Past performance is not indicative of future results. Always consult a qualified financial professional before making any financial decisions.

Frequently Asked Questions

What are the four pillars of fintech?

The four pillars are generally described as digital payments, lending, insurance (insurtech), and wealth management/investment technology. This framing draws from BIS research, though formal taxonomies sometimes include additional categories like capital raising, clearing, and settlement.

How do I know if my current wealth management tools are outdated?

The clearest signals are manual data entry for tasks that could be automated, lack of real-time reporting, poor integration between systems, and clients commenting on communication quality. If any of these feel routine rather than exceptional, the tools have likely outlived their usefulness.

What is the best time to adopt wealth management technology?

When operational inefficiency starts limiting either client capacity or experience quality — not after you've already lost clients or fallen behind competitors. Proactive adoption consistently outperforms reactive adoption, partly because migration is easier when it isn't driven by a crisis.

How does technology improve client relationships in wealth management?

Technology improves relationships by enabling more consistent and transparent communication, including real-time portfolio access and professionally crafted market updates. That consistency builds trust and reinforces the adviser's value beyond investment returns alone.

Can smaller or independent advisory firms benefit from wealth management technology?

Often more than larger firms. Technology allows smaller practices to scale client engagement and delivery quality without adding headcount, closing the gap with more resource-rich competitors. A platform like Scatterplot at $99/month, for example, gives an independent adviser the same presentation quality as a larger team — without the operational overhead.