Introduction

Markets will always move. Sometimes dramatically. What separates advisers who retain clients through rough patches from those who lose them isn't portfolio performance — it's communication.

Many advisers only reach out when markets are already falling, which can be the wrong moment to start the conversation. Clients who haven't been prepared for volatility tend to experience it as a crisis. Clients who have been prepared tend to experience it as expected.

That preparation is a skill — and it's teachable. This guide provides wealth managers and financial advisers with an overview of approaches for explaining market volatility clearly, reducing client anxiety, and turning turbulent periods into trust-building moments. Inside: language guidance, communication frameworks, and visual tools grounded in how clients actually process uncertainty.

This content is for informational and educational purposes only. For guidance specific to your practice or client situations, consulting a qualified financial professional is advisable.

Key Takeaways

- Volatility is normal — normalizing it with clients before markets drop, not during, is an approach many experienced advisers favor

- Client panic is driven by loss aversion and recency bias, not just falling prices

- Advisers who use 4 or more proactive digital touchpoints during downturns are more likely to see clients increase their investments

- Plain language, relatable analogies, and historical context tend to calm clients faster than charts and technical jargon

- Volatile markets can serve as an opening to revisit financial plans and reinforce long-term goals

What Market Volatility Really Means (and How to Define It for Clients)

Most clients hear "volatility" and think "my money is disappearing." That conflation is one of the most common misunderstandings in client-adviser conversations about markets.

Investopedia defines volatility as "a statistical measurement of the degree of variability of the return of a security or market index" — meaning how widely prices swing around their average. The VIX, published by Cboe, measures market expectations of near-term volatility using S&P 500 option prices.

Clients generally don't need to understand the mechanics of either. What tends to be more useful is a clear framing: prices move up and down — sometimes sharply — and that movement is not the same as permanent loss.

Volatility vs. Loss: A Foundational Distinction

This distinction matters significantly in practice. As the CFA Institute notes, the real risk for long-term investors isn't volatility itself — it's the probability of permanent capital loss, which typically only occurs when investors are forced to sell during a decline.

One common way to frame this distinction for clients:

- Volatility = temporary price movement (normal fluctuation around a longer-term trend)

- Loss = what happens when an investor sells at the wrong time, or when a company fundamentally fails

Clients who understand this distinction are generally less likely to make reactive decisions during downturns.

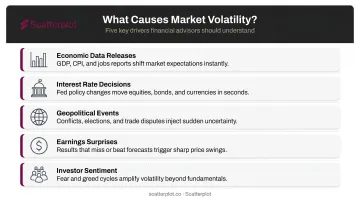

What Causes Volatility (In Plain Terms)

Clients often respond better to causes they already recognize from the news:

- Economic data releases — jobs reports, inflation numbers, GDP figures

- Interest rate decisions — Fed announcements move markets predictably

- Geopolitical events — elections, conflicts, trade disputes

- Earnings surprises — companies reporting above or below expectations

- Investor sentiment — fear and optimism spread quickly, especially in a 24/7 news cycle

Anchoring volatility to familiar headlines gives clients a mental model they can actually use — which can make subsequent conversations easier as well.

Why Clients Panic: Understanding the Psychology Behind Market Fear

When markets drop, clients don't respond to data — they respond to fear. Understanding what drives that fear is central to effective adviser-client communication during volatile periods.

Loss Aversion: Why Losses Hit Harder Than Gains

The foundational research here is Kahneman and Tversky's Prospect Theory. Their 1992 cumulative prospect theory paper estimated a median loss-aversion coefficient of 2.25 — meaning the psychological pain of a loss is felt roughly twice as intensely as the pleasure of an equivalent gain.

Practically, this means a client who sees their portfolio drop by $50,000 feels that loss far more acutely than they felt the pleasure of gaining the same amount. Acknowledging a client's distress rather than minimizing it tends to be more effective, given that the feeling is real even when the loss is temporary.

Recency Bias and the Media Amplification Effect

Recency bias causes clients to overweight recent events when forming expectations about the future. During a downturn, this makes declines feel permanent rather than cyclical. The last few weeks of red numbers become the mental template for what comes next.

Financial media accelerates this effect. Research by Engelberg and Parsons found that local media coverage of market events raised local retail trading volume by 8% to nearly 50% on the days coverage was published. Clients consuming daily financial news aren't getting historical context. They're getting intensity, which tends to drive anxiety and impulsive decisions.

Beyond the Numbers: What Clients Are Really Worried About

Clients aren't just watching a portfolio value. When markets drop, they're watching specific goals feel threatened:

- A retirement timeline they've spent years building toward

- A child's education fund tied to a fixed deadline

- A business or inheritance representing decades of sacrifice

Acknowledging this emotional dimension — not just the financial one — is widely recognized as a key factor in keeping clients engaged through difficult periods. Responding to a panicking client with data alone addresses the financial question but not the underlying concern.

Start the Conversation Before Volatility Hits

A well-established principle in financial communication is that the most effective volatility conversation is one that took place before anything went wrong.

J.D. Power's 2020 investor satisfaction study found that advisers using 4 or more digital touchpoints — email, text, video, or online — were 50% more likely to see increased client investment than advisers who initiated no digital contact. The data suggests that staying in contact before a crisis changes how clients behave during one.

How to Frame the Volatility Conversation During Calm Periods

At onboarding and at annual reviews, many advisers walk clients through their portfolio's potential downside risk — showing them, concretely, what a difficult year could look like, not as a warning, but as a planning exercise.

When clients understand and agree to a potential range of outcomes during a calm moment, they've made a psychological contract with themselves. When volatility actually arrives, that prior agreement can serve as an anchor.

Illustrative framing during stable markets:

- "We've built this portfolio to handle years like 2020 or 2022 — let me show you what that looked like."

- "If markets fell 20% over the next 12 months, here's what your plan would still be able to do."

Segmented Outreach: Not Every Client Needs the Same Message

That framing works best when it's targeted. Client relationship management tools can help identify clients most likely to benefit from early, proactive contact during volatile periods:

- Clients with higher-risk allocations than their temperament suggests

- Clients who have called in distress during previous downturns

- Clients approaching retirement with concentrated equity exposure

- New clients who haven't yet experienced a significant drawdown with you

These client segments are often the ones who reach out in distress — proactive contact ahead of volatility is one approach advisers use to get ahead of that dynamic.

Regular Touchpoints That Build Resilience Over Time

Identifying which clients to reach is one part of the equation. The channels below illustrate how advisers commonly maintain ongoing communication before a downturn tests client relationships:

- Quarterly review meetings that include a brief market context discussion

- Market outlook emails sent during calm periods, not just when things drop

- Client webinars on historical market cycles and how portfolios are designed to handle them

Research and practitioner experience both suggest that multiple conversations before volatility arrives tend to produce better outcomes than a single conversation after it does.

What to Say (and What Not to Say) When Markets Get Rocky

Lead With Empathy, Not Data

When a client calls during a downturn, the instinct can be to explain. Many communication frameworks, however, suggest that clients in an emotional state are generally less able to process information until they feel heard first.

Starting with open-ended questions is a commonly recommended approach:

- "How are you feeling about what's been happening in markets?"

- "What's on your mind since you saw the news this week?"

Language That Calms Without Dismissing

Phrases that tend to be less effective in these conversations:

- "Don't worry" — dismisses the concern without addressing it

- "It's just noise" — can feel condescending when a client's portfolio is down meaningfully

- "This always happens" — may sound glib and feel inaccurate in the moment

Grounding language that many advisers find more effective:

- "This kind of movement is something we planned for."

- "Your portfolio was built with periods like this in mind."

- "We've seen this before, and your plan accounts for it."

Analogies That Work

Analogies tend to calm anxious clients faster than technical explanations of standard deviation. A few commonly used ones:

- The weather analogy: Your financial plan is built for all four seasons — not just the sunny ones. A cold winter doesn't mean spring isn't coming.

- The road trip analogy: We planned a route knowing there would be some traffic. We don't change the destination because of a jam.

- The balloon analogy: Markets inflate, deflate, and inflate further over time. What we're watching right now is one exhale.

The most effective analogies are often ones tailored to what a specific client cares about. An adviser who knows a client is a keen gardener can explain market cycles in terms of seasons. The more personal the reference, the more it tends to land.

Handling the "Should I Go to Cash?" Question

Once emotional grounding is established, this question commonly surfaces. A frequently used response framework:

- Explore re-entry, not just exit: "If we move to cash now, when would we move back in? What would tell us it's the right time?" Most clients find this difficult to answer — which can itself be illuminating.

- Quantify the cost of sitting out: Fidelity research shows that missing just the 5 best market days since 1988 could have reduced long-term gains by 38%. Those best days often follow immediately after the worst ones.

- Consider a middle ground: For clients who want some sense of control, a modest shift toward less volatile assets — without exiting equities entirely — is one approach some advisers discuss as a way to provide psychological relief without significantly disrupting a long-term strategy.

Note: Any specific portfolio changes involve individual circumstances and tax implications. Readers are encouraged to consult a qualified financial professional before making investment decisions.

Use Visuals and Historical Data to Anchor Client Confidence

Historical context is one of the most widely used tools in adviser-client communication. It doesn't predict the future, but it can make the present feel less unprecedented.

The Data That Matters Most

Historical market data shows that the S&P 500 has recovered from every major drawdown in modern history:

| Drawdown Event | Peak-to-Trough Decline | Recovery to New High |

|---|---|---|

| Dot-com bust (2000–2002) | -49.1% | May 2007 |

| Financial crisis (2007–2009) | -56.8% | March 2013 |

| COVID crash (2020) | -33.9% | August 2020 |

The 2020 recovery took roughly six months. The 2009 recovery took over four years. Both recovered. That variability matters. It tells clients that recoveries are real but not always fast — a more honest message than blanket reassurance, and one that tends to hold up better when the timeline extends. Past performance, of course, is not indicative of future results.

The "Zoom Out" Effect

Showing a client their portfolio or a benchmark index on a 30-day chart makes a recent decline look alarming. Showing them a 10- or 20-year chart, and the same decline appears as a small dip in a long upward trend.

The choice of time horizon changes the emotional register of the conversation almost immediately. Same data, different frame.

Where Scatterplot Comes In

One of the practical challenges advisers face during volatile periods is time. Sourcing current market data, building charts, and formatting professional slides takes hours that could be spent with clients.

Scatterplot addresses this with a library of daily-updated market slides, customized with each adviser's logo, colors, and compliance disclosures. Whether walking into a scheduled quarterly review or an unplanned call triggered by a market drop, advisers can arrive with current visuals and guided talking points already prepared.

That kind of consistent, on-brand communication matters most when clients are anxious — because how an adviser shows up in those moments shapes the long-term relationship.

Turn Volatility Into a Planning Opportunity

Volatility doesn't have to be a defensive conversation. Many advisers use it as a prompt to do productive planning work.

Approaches Commonly Used During Volatile Markets

- Tax-loss harvesting: Selling positions at a loss to offset gains is one strategy some investors consider during downturns. The IRS allows up to $3,000 in capital losses deducted annually, with unused losses carried forward. Tax situations vary widely — consulting a tax professional is advisable before taking action.

- Rebalancing: When market swings have overweighted one asset class relative to another, rebalancing toward target allocations is an approach some advisers discuss with clients.

- Revisiting cash flow needs: For clients with large near-term expenses such as tuition or a home purchase, reviewing whether a portion of assets is positioned appropriately for that timeline is a common planning conversation.

These types of conversations give both adviser and client a sense of productive agency — a meaningful alternative to simply watching and waiting.

Reinforce the Long-Term View

Volatile markets are a natural prompt to reconnect clients to why their plan was built the way it was. A well-constructed financial strategy isn't designed for smooth years only — it's typically built with the expectation that rough periods will occur.

An adviser's role in these moments is often less about predicting what markets will do next and more about helping clients remain committed to a plan that already accounts for uncertainty.

Disclaimer

The content on this site is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. It should not be relied upon as the basis for any investment decision. Past performance is not indicative of future results. Always consult a qualified financial professional before making any financial decisions.

Frequently Asked Questions

What is market volatility in simple words?

Market volatility refers to how frequently and how sharply investment prices move over a short period. It's a normal feature of financial markets, not a sign that something has gone permanently wrong, and it affects prices in both directions.

How do I explain market volatility to clients?

Plain language and a relatable analogy, combined with validation of how clients are feeling and historical context, are approaches many advisers find effective. Markets have recovered from every major downturn on record — connecting that historical pattern back to a client's specific financial plan and goals can be a useful framing. This is general communication guidance; individual client conversations may vary based on specific circumstances.

What should you not say to clients during market volatility?

Dismissive phrases like "don't worry" or "it's just noise" can feel invalidating. Making specific predictions about when markets will recover, or guaranteeing outcomes, are also approaches widely regarded as both unhelpful and potentially problematic from a compliance standpoint.

How often should advisers reach out to clients during volatile markets?

Proactively, and in order of priority, is a common recommendation. Higher-anxiety or higher-risk clients are often the first to be contacted. Regular, brief check-ins during volatile periods — even a short email — are generally regarded as more effective than waiting for clients to reach out in distress.

Should clients change their portfolio during a volatile market?

Portfolio decisions during volatility depend heavily on individual circumstances, goals, time horizon, and risk tolerance. In general, dramatic changes based on short-term movements are something many financial professionals caution against. Modest rebalancing or small adjustments can sometimes provide a sense of control, but the appropriateness of any change depends on a client's specific situation. Consulting a qualified financial professional is the most reliable way to evaluate options.