The CFP Board's curriculum spans 8 principal knowledge domains and 70 topic areas. No advisor reliably holds all relevant rules, exceptions, and interactions in working memory across every client situation.

Checklists and flowcharts address this directly. They've transformed quality control in medicine and aviation — and they're now becoming essential infrastructure for advisors who want to deliver consistent, comprehensive advice at scale.

This guide covers why these tools matter, when to use each, which ones every advisor needs, and how to build them into a repeatable client service process.

Key Takeaways

- Checklists reduce errors and omissions by ensuring every critical planning question gets asked — every time

- Flowcharts handle conditional decisions better (Roth eligibility, Social Security claiming, RMD rules)

- Advisors need checklists for four lifecycle stages: onboarding, annual review, life events, and retirement transitions

- A client service calendar built around monthly checklist themes creates structured, year-round engagement

- Pairing planning visuals with daily-updated branded market slides turns routine reviews into trust-building conversations

Why Financial Advisors Need Checklists and Flowcharts

The Two Ways Advisors Fail Without Structure

Financial planning complexity has grown well beyond what any advisor can track mentally across dozens of client relationships. The CFP Board's curriculum covers 8 principal knowledge domains — from tax planning and retirement income to estate planning and insurance — each with its own rules, thresholds, and exceptions that interact with one another.

This creates two distinct failure modes:

- Errors — applying a rule incorrectly because a relevant interaction was missed

- Omissions — failing to ask a question that would have revealed a critical issue

A concrete example of the second: an advisor reviews Social Security claiming strategy without asking whether the client had non-FICA earnings from a government pension. That single missed question means the Windfall Elimination Provision — which could significantly reduce their benefit — never enters the analysis. The client gets a plan built on incomplete information.

The Evidence for Structured Tools

The medical parallel is hard to ignore. A 2009 NEJM study of a 19-item WHO surgical checklist across 8 hospitals found death rates fell from 1.5% to 0.8% and inpatient complications dropped from 11.0% to 7.0%. These weren't inexperienced surgeons — the checklist worked because it ensured consistent application of knowledge under pressure, not because it taught anyone something new.

Advisors face the same challenge. Expertise isn't the gap; consistent execution across complex, high-stakes conversations is.

The Business Case

Beyond error reduction, standardized planning processes deliver real practice management advantages:

- Onboard associate advisors faster with documented workflows

- Maintain advice quality across a growing client book

- Satisfy compliance expectations more easily — FINRA Rule 2111 and SEC Reg BI both require advisors to demonstrate reasonable diligence and a sound basis for recommendations

- Show clients the depth of what's being managed on their behalf, which builds trust and perceived value

Checklists vs. Flowcharts: Knowing When to Use Each

These tools solve different problems. Using the wrong one for a given situation creates friction rather than clarity.

What Each Tool Does Best

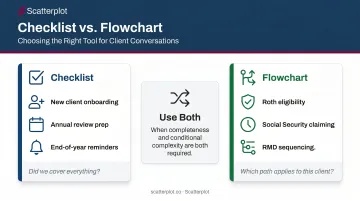

A financial planning checklist is a linear, sequential list of items to verify or complete. It's best suited for scenarios where the same set of questions applies to nearly every client — new client onboarding, annual review prep, end-of-year planning reminders. Checklists excel at ensuring completeness.

A financial planning flowchart is a decision-tree visual that branches based on yes/no answers or conditional criteria. It's best for scenarios where the correct path depends on specific client facts. "Can this client make a deductible IRA contribution?" requires branching through income, filing status, and workplace plan participation — a checklist can't handle that cleanly. Flowcharts also carry a client education benefit: walking someone through the decision tree shows exactly why a particular path applies to their situation.

The Quick-Reference Rule

| Goal | Use |

|---|---|

| "Did we cover everything?" | Checklist |

| "Which path applies to this client?" | Flowchart |

| Both completeness and conditional complexity | Use both |

An annual review, for example, pairs well with both: a checklist to confirm every topic was covered, and a Roth conversion eligibility flowchart to work through the clients where that decision actually branches.

Must-Have Financial Planning Checklists Across the Client Lifecycle

New Client Onboarding

A thorough onboarding checklist should capture two layers of information.

Document collection:

- Investment and retirement account statements

- Two to three years of tax returns

- Insurance policies (life, disability, long-term care, umbrella)

- Estate documents (will, trusts, powers of attorney, healthcare directives)

- Outstanding liabilities and debt schedules

Qualitative inputs:

- Risk tolerance and investment experience

- Short- and long-term goals

- Family structure and any anticipated changes

- Life transitions in the near horizon (retirement, job change, sale of business)

This sets the foundation for a comprehensive plan and reduces the risk of missing a material issue in year one. There's a client experience benefit too: seeing the breadth of what their advisor covers signals professionalism — and clients who feel that thoroughness early are more likely to engage fully from the start.

Annual Review and Life Event Checklists

Portfolio performance is just one line item. A complete annual review checklist covers:

- Beneficiary designations on all accounts and insurance policies

- Insurance adequacy (life, disability, long-term care)

- Tax return review and year-over-year comparison

- Estate plan currency — only 24% of Americans have a will, according to Caring.com's 2025 study, down from 33% in 2022

- Retirement contribution maximization (including catch-up eligibility)

- Changes in personal or financial situation since the last meeting

The same Caring.com research found that 62% of people with estate plans updated their documents within the last five years, with triggers including property purchases (30%), family expansion (23%), and medical diagnoses (10%). These are exactly the life events advisors should be asking about proactively — not waiting for clients to bring them up.

Structured annual reviews also open the door to a deeper engagement model. Mid-year and event-triggered checklists keep advisors in front of clients at the moments that matter most:

- March–April: Tax return review

- May–June: Investment and portfolio review

- September–October: Insurance coverage assessment

- November–December: Year-end tax planning opportunities

Life event scenario checklists every advisor should have ready:

- Approaching retirement

- Job change or severance

- Marriage or divorce

- Death of a spouse

- Receiving an inheritance

When a client calls about a job loss or an unexpected inheritance, having a pre-built scenario checklist means you're guiding the conversation — not scrambling to remember what to ask.

Using Flowcharts to Navigate Complex Planning Decisions

Where Flowcharts Add the Most Value

Some planning topics have enough conditional complexity that a linear checklist simply can't capture the decision logic. Flowcharts are the right tool when the correct answer depends on a specific sequence of yes/no decisions based on client facts.

The highest-value flowchart topics for most practices:

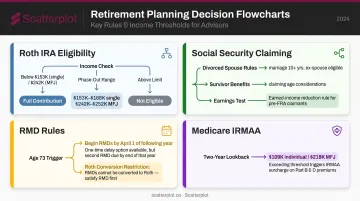

- Roth IRA eligibility and backdoor Roth contributions — For 2026, the phase-out range is $153,000–$168,000 for single filers and $242,000–$252,000 for married filing jointly. A single income figure changes the entire strategy.

- Social Security claiming — Divorced spouse rules, survivor benefits, the Earnings Test, and the now-repealed Windfall Elimination Provision (eliminated for benefits payable January 2024 and later under the Social Security Fairness Act) each require conditional branching.

- RMD rules and delay strategies — The first RMD applies in the year the account owner reaches age 73, with an option to delay until April 1 of the following year. RMD amounts cannot be converted to Roth — a fact that changes Roth conversion sequencing.

- Medicare IRMAA thresholds — For 2026, Part B surcharges begin above $109,000 for individual filers and $218,000 for married filing jointly. A Roth conversion that pushes income across a bracket triggers a two-year lookback surcharge, which a flowchart makes visible before the decision is made.

Flowcharts as Quality Control in Multi-Advisor Practices

When a newer associate follows the same decision tree as a senior advisor, variance in recommendation quality shrinks. This matters for compliance oversight too — the flowchart creates a documented, logical record of how a recommendation was reached, which supports the reasonable diligence standard under FINRA Rule 2111 and SEC Reg BI.

That same logic extends to the client-facing conversation. A Roth conversion flowchart carries more weight when the advisor can also show the current rate environment or market valuation backdrop — the planning decision and the market context reinforcing each other in one meeting.

Platforms like Scatterplot deliver daily-updated, branded investment charts that slot directly into that workflow, so the planning logic and market context land together rather than in separate, disconnected conversations.

Building Your Annual Client Service Calendar

The client service calendar is a structured, year-round plan that assigns specific planning topics to different months — ensuring every client receives proactive outreach on relevant issues throughout the year, not just at an annual review.

Cerulli research found that 55% of advisors consider new client acquisition a challenge — and that 1 in 4 advised clients don't understand their fee structure. Regular, structured outreach tied to concrete planning topics addresses both problems: it demonstrates ongoing value and makes the advisor's work visible.

A Sample Monthly Calendar Framework

| Month | Planning Theme | Tool |

|---|---|---|

| January–February | Savings strategy, contribution limits | Checklist |

| March–April | Tax return review | Checklist + flowchart |

| May–June | Investment and portfolio review | Flowchart |

| July–August | Estate plan review | Checklist |

| September–October | Insurance coverage assessment | Checklist |

| November–December | Year-end tax planning | Flowchart |

Sending a relevant checklist or flowchart with each monthly touchpoint email makes the advisor's work tangible. Clients see exactly what's being tracked on their behalf.

That visibility compounds when those tools are consistently branded. When planning checklists, market slides, and client decks all carry the same logo and color scheme, the result is a cohesive service experience — not a stack of generic documents from different sources.

Disclaimer

The content on this site is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. It should not be relied upon as the basis for any investment decision. Past performance is not indicative of future results. Always consult a qualified financial professional before making any financial decisions.

Frequently Asked Questions

What is the difference between a financial planning checklist and a flowchart?

Checklists are linear and task-based : they ensure completeness by confirming every relevant topic was covered. Flowcharts are branching and visual : they guide conditional decisions where the right answer depends on specific client facts. Many planning scenarios benefit from both tools used together.

What is the 80/20 rule for financial advisors?

According to InvestmentNews, roughly 80% of an advisory firm's revenue typically comes from 20% of client households. The same principle applies to planning tools: a focused set of well-built checklists and flowcharts covers the vast majority of recurring client scenarios, delivering outsized returns on the time spent building them.

How often should financial advisors update their planning checklists?

At minimum, checklists should be reviewed annually and immediately after any major tax law or regulatory change. Thresholds for Roth contributions, IRMAA brackets, RMD ages, and contribution limits change regularly — an outdated checklist can produce incorrect guidance.

Can financial planning checklists be shared directly with clients?

Yes. Client-facing checklists and flowcharts help clients understand the scope of their plan, feel engaged in the process, and appreciate the complexity their advisor manages on their behalf. Branded versions reinforce advisor value and make a strong impression.

What is a red flag for a financial advisor?

Common warning signs include skipping discovery questions, failing to document recommendations, or being unable to explain the reasoning behind a strategy. Structured checklists and flowcharts address these concerns directly, creating a consistent, transparent, and documented planning process.